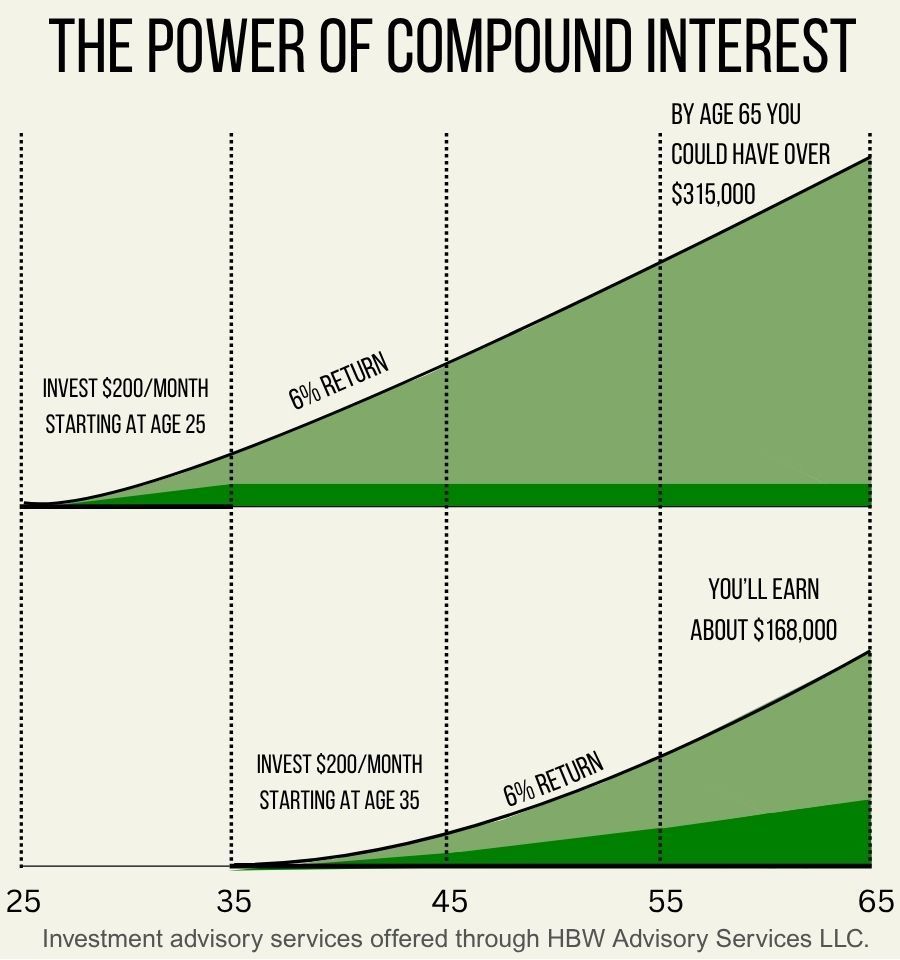

That 10-year delay more than cuts your outcome in half. That’s the silent cost of waiting.

The longer you wait, the harder it becomes to catch up—and the more pressure you’ll feel later in life to increase your savings rate dramatically.

Why We Procrastinate—and Why It’s So Common

Financial procrastination isn’t about laziness—it’s about uncertainty. Many people don’t know where to begin, worry they don’t have “enough” to start, or believe that retirement planning is something they’ll deal with “someday.” Add in confusing terminology, financial jargon, or fear of making the wrong move, and it’s no wonder so many put it off.

You’re not alone if you’ve ever thought:

- “I’ll start once I make more money.”

- “I don’t have enough to make a difference.”

- “It’s too late for me to catch up.”

These are incredibly common thoughts—but they’re also incredibly limiting. The truth is, starting with what you have—even if it’s small—can shift your entire financial trajectory. And the sooner you start, the more flexibility and freedom you’ll have down the road.

Why People Wait—and How a Fiduciary Advisor Can Help

Many people delay saving because they’re unsure where to start or feel overwhelmed by too many options. Workplace retirement plans—whether it’s a 401(k), 457, or 403(b)—can be confusing, especially when salespeople push products that aren’t always in your best interest.

That’s where a fiduciary financial advisor comes in. Fiduciaries are legally required to act in your best interest, not their own. Unlike commission-based representatives who may steer you toward annuities or other high-fee products, a fiduciary helps you make clear, strategic decisions for your future.

If you’ve ever felt unsure about the terms in your retirement plan—especially if you’re in a 403(b) or TSA (tax-sheltered annuity)—you’re not alone.

This previous post dives deeper into how misleading product labels and long surrender periods can quietly eat away at your financial flexibility.

A fiduciary advisor will:

- Tailor your plan to your goals and timeline,

- Help you avoid costly mistakes,

- Show how even small steps today can lead to a more secure future.

It’s about clarity, not confusion. Strategy, not sales.

Start Sooner, Retire Stronger

You don’t need a perfect financial situation to get started—you just need to start. Even the smallest shift, like increasing your contribution by 1% or setting up an automatic monthly investment, can create positive momentum.

The key is to take control now, rather than leave it to “someday.” A fiduciary advisor can help you clear the fog, make confident decisions, and build a retirement plan that works for you—not someone else’s sales quota.

Want to take that first step? Contact Bradford Financial Advisors today—our team is here to help you turn today’s small changes into tomorrow’s financial freedom.

Investment advisory services offered through HBW Advisory Services LLC